Today we have a guest post from our friend Mark of Bare Budget Guy. Enjoy!

Today we have a guest post from our friend Mark of Bare Budget Guy. Enjoy!

If you are like most people, just hearing the word “investing” makes you little bit uncomfortable. It’s sort of like when my 3 year old daughter asks me to do her hair. When it comes to that, I have no idea what I’m doing, and frankly I’d prefer that someone else do it.

But the scope of investing is much broader than doing pig tails on a 3 year old girl. It encompasses so many different things.

The good news is that you do not have to know everything about investing. You don’t even have to know most everything. In fact, you don’t have to know much at all. All you need is some simple foundational knowledge that you can use to decide what kind of investor you want to be.

Investing becomes much less intimidating when we focus on its simple purpose: to generate a profit.

That’s all it is. We put our money to use in order to earn some kind of return on that money.

How we put it to use is where all the confusion comes from. Investing can yield you a profit (or loss) from something as simple as putting your money in a savings account or from something as complex as owning mortgage-backed securities.

If you are like me, however, your eyes glaze over a little bit when you start hearing about stocks, bonds, options, futures, gold, real estate, etc. If you find that those things bore you, don’t worry about it…yet.

Investment hierarchies

You should be aware of the concept of an investment hierarchy. An investment hierarchy is simply a recommended order (or levels) of investment categories. For example, you should generally not invest in mutual funds before you have some short-term cash savings, and you should not max out your retirement accounts before you have an emergency fund in place.

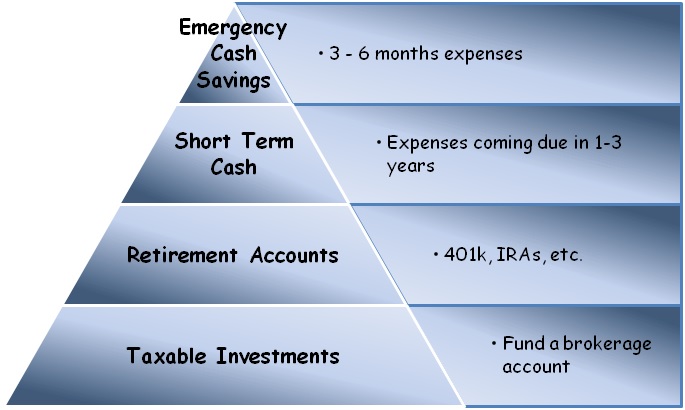

A simple investment hierarchy

There is no one-size-fits all, but here is a general guide.

1) Emergency Cash Savings – 3 to 6 months

2) Short Term Cash – Expenses coming due in 1 to 3 years

3) Retirement accounts – 401k, Roth IRA, etc.

4) Taxable Investments – Fund a brokerage account

Level 1: The Emergency fund

Your emergency fund dollars should be held somewhere you have quick access to like a savings or money market account. The amount should be enough to cover 3 to 6 months of fixed expenses.

You do not touch this money unless you have an emergency. It is not to be tapped for vacations, new roofs (unless it was destroyed in an unexpected tornado), new cars, etc.

For my family of 5, we currently have an emergency fund of $30,000. It’s more than 6 month’s worth (probably closer to 8), but if you value a little bit of extra security and peace of mind, it may be worth it to you to be more conservative.

Level 2: Short Term Cash

This is what I like to call my spend fund. In addition to emergency cash savings, cash should be available for future short-term expenses such as down payments on a home, car purchases, or that air conditioning unit you know you’ll have to replace within a few years.

We have a short term cash savings of $10,000, which will hopefully cover any repairs or major maintenance within the next year or two.

Level 3: Retirement accounts

The main reason people invest in retirement accounts like 401ks or IRAs are because of the attractive tax breaks and employer matches. It makes sense to invest the maximum amount if you can in order to realize the full benefit.

The limit is there because the government is actually foregoing revenue by giving you tax breaks that encourage savings. It’s almost like they are lending you the taxes due on the money you choose to save.

If you have a 401k or similar plan through your employer, definitely contribute what your employer is willing to match. Some advisors recommend contributing the minimum to get the match, then fully funding a Roth IRA, and then coming back to max out your 401k if possible. That assumes that the IRA has lower maintenance fees and more flexibility, which may or may not be the case.

I have to contribute 5% to get the full company match that my company offers. When I joined my company a few years ago, I contributed just enough to get the match and put any extra toward paying off my school debt. Once the debt was paid off, we increased the 401k contribution to 15%.

Level 4: Taxable investments

This is where all those scary words come into play. Hold your breath, and it will be over soon.

There are two general types:

- Stocks (also called equities) – Buying a stock makes you a part owner of a business. You can earn a return through dividends (profits the company gives to the owners) or on the sale of a stock that has appreciated in value.

- Bonds (also called debt investments)- When you buy a bond, you are lending your money. In return, you collect interest and eventually recover the principal as well.

Mutual funds and index funds can be collections of both stocks and bonds and are usually managed by brokerage firms like Charles Schwab or Fidelity. Most investors don’t go beyond this point.

More sophisticated investors mess around with things like options, futures, precious metals, derivatives, etc. These types of investments are much more complex and speculative. They are generally high-risk securities that have the potential for higher returns, but if you don’t have your investment foundation in place, don’t even think about gambling with these.

Okay, you can let it out now, we’re done with that part. Unless you have levels 1-3 in place, there is not much need to focus here unless you’re interested.

Some people have found that once they learn the basics of the debt & equity markets that they actually enjoy this area of the world of investing. So don’t write it off just yet. It’s at least good to be aware of in case you ever have a change of heart.

Customize your investment hierarchy

More good news is that you have a lot of flexibility in how you invest.

I do not max out my retirement accounts. Why? I don’t have enough money.

Let me rephrase that: I have other investments that take priority over maxing out my retirement accounts.

If I maxed out my retirement account, I wouldn’t have enough left over to invest in my kids’ education funds. I recently opened up 529 plans for each of my 3 kids, and I try to put about $500 toward those each month.

Any leftover cash still doesn’t go toward my 401k (Level 3) or any brokerage accounts (Level 4). It actually goes toward my mini-retirement fund! That is a whole separate topic, but the point is to learn some general investing frameworks and to do what works for you.

Remember your objective

Don’t get so caught up in the hierarchy, however, that you forget the whole premise of investing. It’s to earn a return. In other words, to make more money!

Why do you want more money? Probably because you think it will give you access to things that will contribute to your happiness like freedom, peace of mind, or the ability to travel with (or without) family. Focusing or worrying excessively about your investment portfolio will produce the opposite of effect of your original goal — to be happy.

Why is the thought of investing intimidating to you? What do you think about the idea that investing can be a vehicle for greater happiness?

Check out some of our favorite personal finance resources:

Are you getting the best credit card rewards? Check out the top cash back credit card offers (updated daily)

Make extra money: 15 ways to make money from your computer

Get the First Chapter Free!

Join our online community and get the first chapter of the book Student Loan Solution absolutely FREE!

So far, we’re comfortably through Level 3. Level 4 is where I start to feel like I’m in the deep end of the pool. This guide is helpful, though!

This is solid, practical advice. Even if you don’t understand everything about investing, it’s wise to start saving/investing what you can now and then educate yourself and learn more as you go along!

These are really smart tips. I am actually more inclined to prioritize level two above level one, since they are known expenses, but having the e-fund in place is probably more intelligent.

Oh, and in level 4, you forgot about my favorite class of investments- Real Estate!!!

I’ve never seen this laid out in this way before, but I like it! I don’t typically think of emergency savings or cash savings as investments though. I think for many people the most intimidating thing about investing is all of the options available, and the fact that there are so many professionals out there telling you how to invest. Many people probably think that they can’t do what the professionals can, but the truth is that it is not that complicated! Invest in low fee index funds for the long term. Done.

I really like the way you laid this out, the pyramid visual really makes this a lot simpler to understand! We’re pretty good through level 3, and then we start to get intimidated by further ways to invest our money. This is one of my goals for the next few months is to figure out a new investing strategy!

Thanks Christina! If you’re at three then you are in good shape. I think people at that level are winning with money. Getting into level four is about winning even more :)

That’s my approach! I think that’s the problem. People think investing means they have to be a hedge fund manager, when in reality its about starting simple and maybe getting into some no load index or mutual funds.

Real Estate would definitely fall in that level. There is actually a whole other pyramid within level 4, but it’s probably not worth worrying about for most people.

That is exactly right. Start with what you know, make progress, and educate yourself along the way!

There are some pretty helpful free “investing 101” guides out there. All it takes is a quick google search, and you can be more educated than your average investor.

Welcome to the mix Mark! Agree on the hierarchy and that you certainly don’t need to know everything.. Although I enjoy learning more about personal finance, investing etc

I feel it can be a vehicle for greater happiness however it’s really for me about understanding why you want to invest and what for

Cool article here though! :)

I love this hierarchy! I never thought of it like that, but it makes a ton of sense. Especially for those of us who have to prioritize our savings each month! :)

Good article. I am in the party of those who actually enjoy the investing process. I recently started writing a series on investing in stocks. I agree with your premise of having an investment hierarchy, but I also believe that if you can teach yourself to specialize in a certain area of investment – whether it’s real estate, stocks, commodity futures, etc. – you may be able to magnify your returns. While that is a risky move, if you do your homework, you should be able to come out on top. “All eggs in a few baskets, and watch it closely” cliché.

Love the levels and the articles but can’t help but think the pyramid is upside down… For one to build on another the most basic and first level should be at the bottom and the next build on it above and so forth…

This is a great way to look at your investment structure as a “hierarchy”. I think it’s important to have emergency and liquid savings in place before you begin your retirement or taxable investment accounts. A good financial foundation should always be in place before a portfolio is set up.